- 2025-08-22

- Category: Money & Well-Being, Risk & Protection

Loans for Recovery After Technogenic Accidents

When a technogenic disaster strikes — think of oil refinery explosions, chemical leaks, train derailments, or large-scale industrial fires — the damage goes far beyond the immediate area. Lives are disrupted, ecosystems may be poisoned, and businesses come to a halt. Infrastructure collapses under the strain. Yet amid the chaos, one urgent question always arises: who pays for the damage, and how fast can recovery begin?

Loans have become an indispensable tool in this context. Whether it’s private companies trying to restart operations or governments scrambling to restore critical infrastructure, credit allows recovery to begin even before investigations end or insurance disputes are resolved. But as useful as they are, these loans come with challenges, terms, and long-term consequences. Understanding how this financial bridge works can shape faster and smarter disaster responses in the future.

Why Loans Are Often the First Step

Unlike natural disasters, which often trigger immediate insurance claims and government relief funds, technogenic accidents tend to get stuck in legal and regulatory gridlock. Investigations into fault and compliance can take months. Insurers may delay payouts. Regulators often demand audits and reviews. But communities and businesses can’t wait. Every day that a power plant stays offline or a logistics hub remains shut down means lost revenue, declining public services, and social frustration.

Loans offer a way to move forward despite the legal fog. For businesses, they cover urgent needs — restarting production, repairing broken equipment, managing payroll, or rehiring laid-off workers. For municipalities, loans mean roads can be reopened, clean water restored, or emergency shelters expanded. In short, credit speeds up recovery when other systems are too slow to react.

What Kinds of Loans Are Typically Used?

Post-disaster lending isn’t one-size-fits-all. Different actors use different financing tools depending on the sector, scope, and urgency of recovery. Some loans are short-term, bridging the gap until insurance or litigation is settled. Others are long-term, funding major infrastructure rebuilds over decades. Here are some of the most common:

- Emergency Operating Loans: For businesses needing immediate liquidity to survive the first 60–90 days after the event.

- Infrastructure Rehabilitation Loans: For public agencies or utility companies rebuilding roads, water networks, or power grids.

- Environmental Cleanup Loans: Especially relevant for events involving toxic spills or contamination that require long-term remediation.

- Safety Compliance Loans: To upgrade safety systems or rebuild facilities in compliance with new regulations imposed post-disaster.

Common Loan Uses Post-Technogenic Disaster

| Loan Type | Sector | Repayment Term |

|---|---|---|

| Emergency Working Capital | Manufacturing, Retail, Logistics | 12–36 months |

| Public Infrastructure Loans | Transportation, Utilities, Health | 10–30 years |

| Remediation & Safety Upgrades | Energy, Mining, Chemicals | 5–15 years |

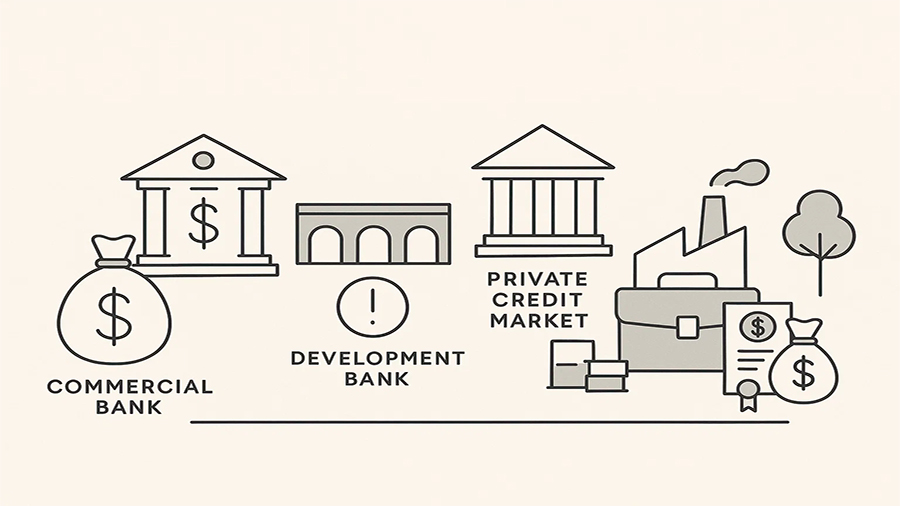

Sources of Recovery Financing

Where does this money come from? It depends. Often, commercial banks provide the first lines of credit to businesses they already know. Development banks — national or international — support larger infrastructure projects or environmental remediation efforts. In some regions, governments have standby relief funds designed to kick in during emergencies. These funds may provide low-interest loans, grants, or guarantees to reduce risk for private lenders.

Private credit markets also play a role, especially for companies with strong reputations or assets to pledge as collateral. However, interest rates and loan conditions vary depending on how risky the lender perceives the borrower to be. A company facing lawsuits or public backlash may struggle to secure favorable terms, even if its operations were otherwise sound before the accident.

Obstacles That Delay or Complicate Lending

Despite the urgent need, securing loans after a technogenic disaster is far from easy. Several barriers can complicate or delay the process:

- Liability Uncertainty: If fault hasn’t been legally determined, lenders may be reluctant to extend large sums.

- Disrupted Financial Records: Damaged facilities may lose digital and paper documents, complicating due diligence.

- Political Scrutiny: Public outcry can lead to heightened oversight, slowing down loan approvals for public projects.

- Legal Battles: If lawsuits are underway, a company’s future cash flow may be in question.

Barriers to Loan Approval and Disbursement

| Barrier | Effect on Lending |

|---|---|

| Ongoing investigations | Freezes credit until fault is determined |

| Unstable cash flow | Raises lender risk, may lead to denial or high rates |

| Public backlash | Delays political approvals, especially for public-sector loans |

| Lack of recovery plan | Prevents financial institutions from assessing feasibility |

How Credit Can Drive Smarter Recovery

The best recovery doesn’t just restore the old — it builds something better. Loans offer a rare opportunity to rethink outdated infrastructure, dangerous industrial practices, or insufficient safety systems. If used strategically, borrowed funds can go beyond repair and drive innovation. Think smart grids instead of just fixing old power lines. Think sustainable transport instead of patching broken roads. It’s not about replacing what was lost — it’s about reimagining what’s next.

For companies, that might mean investing in automation, supply chain redundancy, or improved worker safety protocols. For cities, it could involve modernizing flood defenses, green building retrofits, or investing in early-warning systems. Loans, when deployed with vision, become tools of transformation.

The Human Side of Financial Recovery

Loans may help rebuild factories and roads, but what about people? Workers, families, and small business owners bear the brunt of technogenic accidents. Often, credit programs ignore this human layer. While larger firms may secure millions in recovery funds, local shops or displaced residents are left navigating red tape.

Some innovative programs now include community recovery loans — smaller, faster, and more targeted. These might go to neighborhood stores, freelance workers, or co-ops affected by the disaster. The logic is simple: local economies recover faster when everyone has access to resources, not just the biggest players.

Preparing for Future Disasters

Technogenic risks aren’t going away. If anything, aging infrastructure, climate stress, and digital vulnerabilities are increasing the frequency and scale of such events. That’s why some governments and companies are now creating standby credit frameworks — pre-approved loans or bond facilities that activate automatically after a certified emergency.

Other tools include parametric financing, where funds are released based on predefined triggers — like pollution levels or seismic activity — instead of bureaucratic evaluations. These tools could drastically speed up response times and reduce long-term costs by enabling immediate action. Faster credit means fewer cascading failures.

Conclusion

Loans are one of the few tools capable of kickstarting recovery before all the facts are in. They offer liquidity, momentum, and possibility. But for them to work well, they need to be accessible, flexible, and thoughtfully structured. The future of disaster response will depend not only on our ability to respond logistically — but financially. Technogenic accidents may be unpredictable, but our financing doesn’t have to be.